Capital allocation principles

In March 2024, we conducted a broad capital allocation review, considering the Group's strategy within its reshaped footprint. This review has concluded the following key outcomes:

- Investment: Following an extensive review of our capital investment requirements, the current capital intensity will be broadly maintained at a market level, which will allow for appropriate investment in networks and growth opportunities.

- Leverage: A new leverage policy of 2.25x – 2.75x Net Debt to Adjusted EBITDAaL and we target to operate within the bottom half of this range. The leverage policy supports a solid investment grade credit rating and positions Vodafone to continue to invest for growth over the long-term.

- Shareholder returns (dividends): The Board has declared total dividends of 4.6125 eurocents per share for FY26 (FY25: 4.5 eurocents), reflecting a 2.5% year-on-year increase in line with our commitment to a progressive dividend policy announced in November 2025.

- Shareholder returns (share buybacks): The final tranche of the second €2 billion share buyback programme completed on 11 May 2026. Since the launch of the first share buyback programme in March 2024, we have repurchased 4.2 billion shares. Total capital returns to shareholders in FY26 were €3.1 billion.

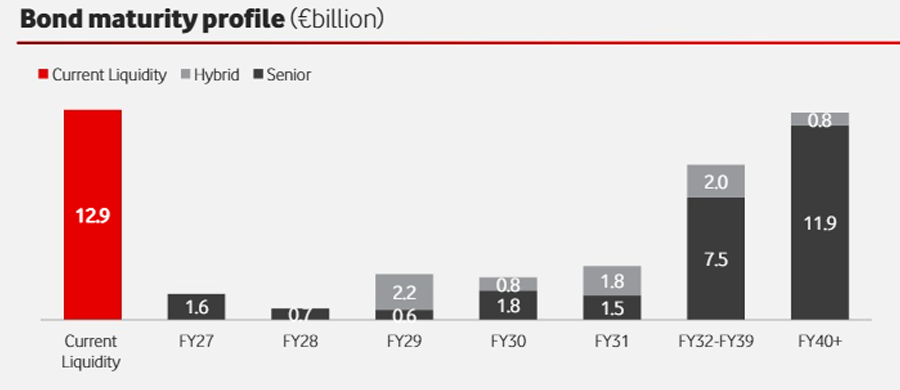

Hybrid bonds

The bond maturity profile includes hybrid securities, the key features of which are:

- Legal maturity of at least 30 years but are callable between FY29 and FY51.

- Attract 50% equity treatment from all three major credit rating agencies (Moody’s, S&P and Fitch).

- A permanent part of our capital structure.

- Treated at 100% debt in our accounts and net debt to adjusted EBITDaL calculation.